NEWS

13 Oct 2025 - Performance Report: Altor AltFi Income Fund

[Current Manager Report if available]

13 Oct 2025 - Performance Report: Argonaut Global Gold Fund

[Current Manager Report if available]

13 Oct 2025 - 10k Words | October 2025

|

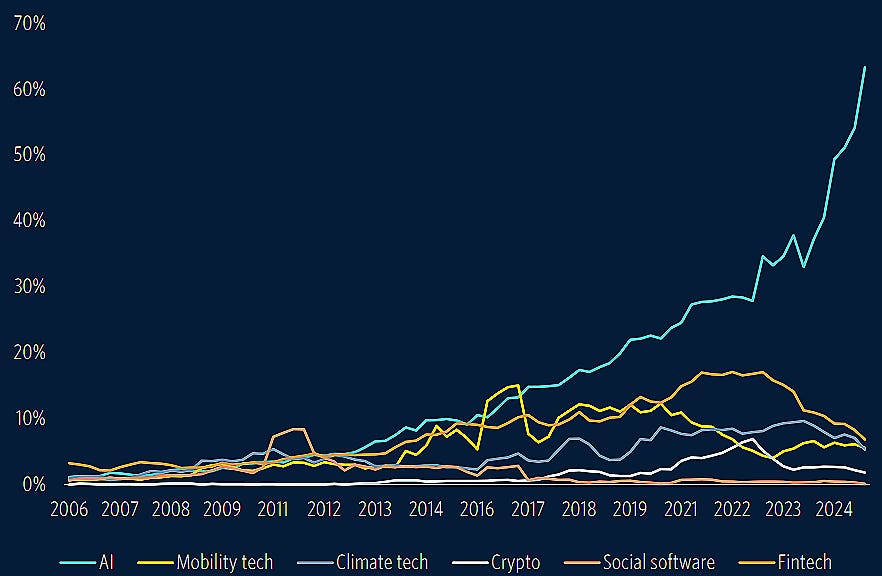

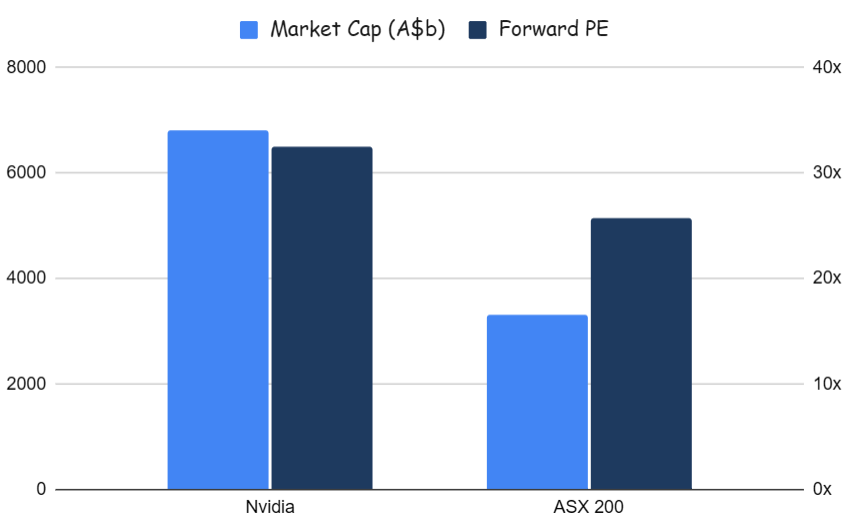

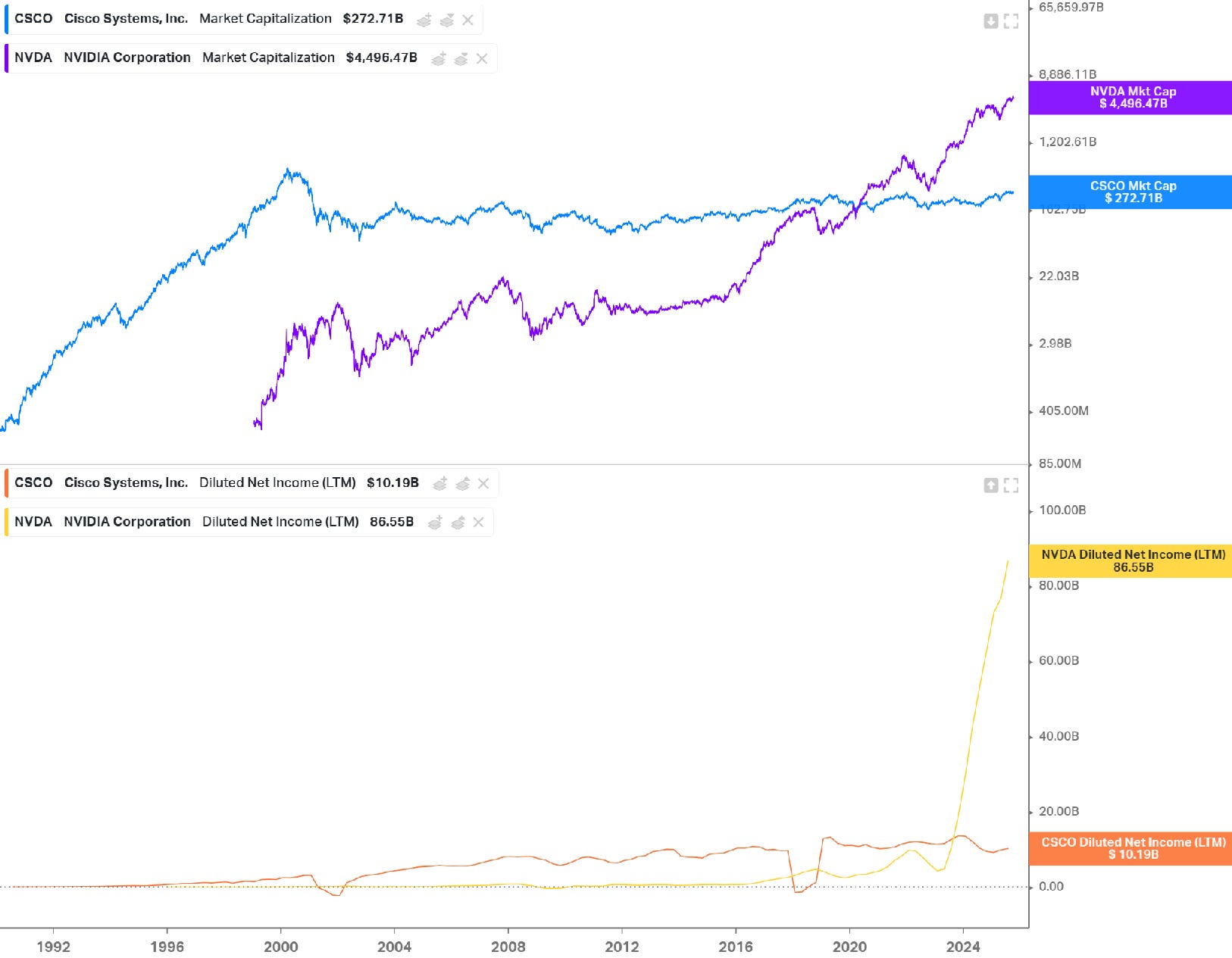

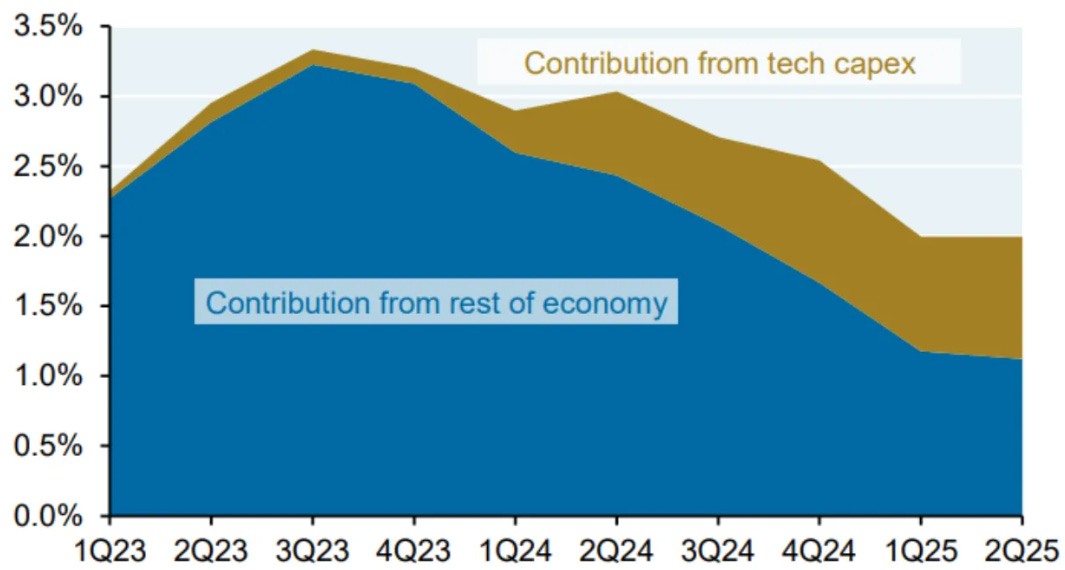

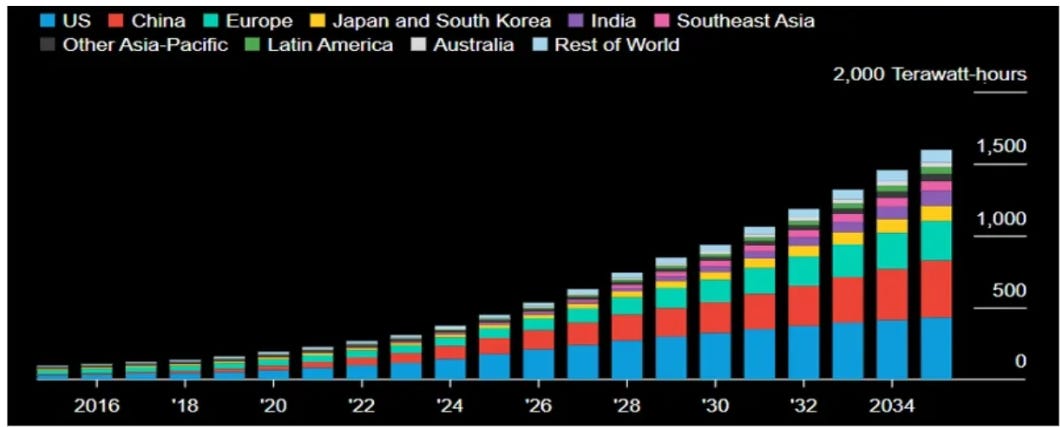

10k Words Equitable Investors October 2025 Small stocks are making up some lost ground with investor interest returning. Size has been the key factor on the ASX over the past 12 months, whereas in the US it has only come to the fore in the past three months. Australian 10 year bond yields have been pretty stable for the past few years but political turmoil in Japan and France shows up in their equivalent bond yields. The extent to which AI is dominating venture funding is unprecedented. But so is the extent to which Nvidia dominates the total value of Australia's top 200 companies. Surging earnings is the difference when comparing Nvidia's valuation to that of Cisco during the dot com boom. The economy is certainly relying more heavily on tech sector capex - and anticipating 4x growth in power demand from AI data centres over the next 10 years. Finally, we still have over 1,000 companies a month entering external administration in Australia, compared to just over 500 a month between FY2020 and FY2023. Record weekly value of trade in S&P/ASX Emerging Companies stocks (5 highest weekly amounts since 2004 v averages)

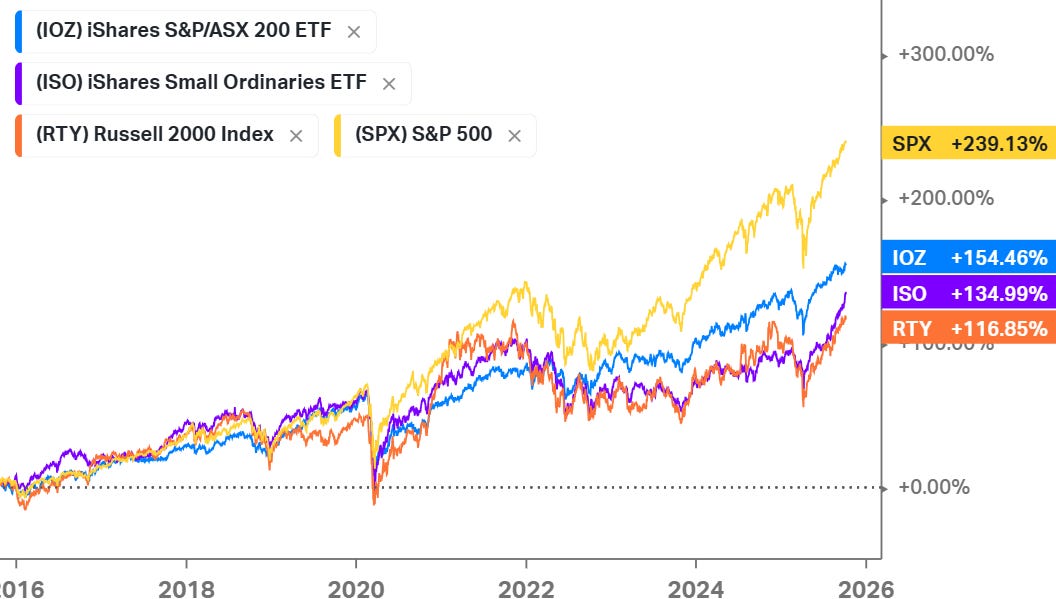

Source: Equitable Investors, Iress One year returns - Australian small caps leading large caps in Aus and US

Source: Koyfin Ten year returns - small caps still lagging

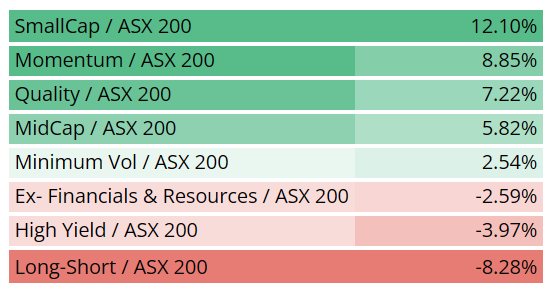

Source: Koyfin ETF-based factor analysis highlgiths size as the key on the ASX over the past 12 months

Source: Equitable Investors US factor ETF performance / S&P 500 ETF performance over past 3 months

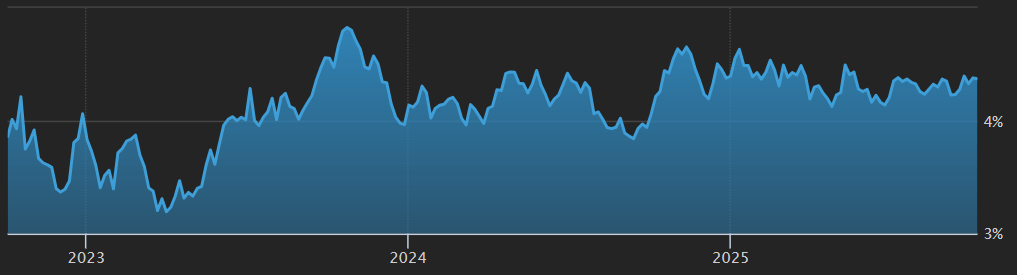

Source: Koyfin 10 year Japanese government bond yield

Source: WSJ.com 10 year French government bond yield

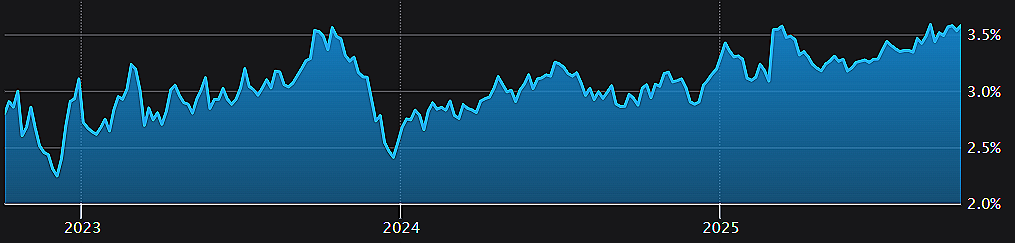

Source: WSJ.com 10 year Australian government bond yield

Source: WSJ.com AI's share of value of venture deals over trailing 12 months

Source: PitchBook Nvidia's market cap and PE multiple relative to the S&P/ASX 200

Source: Equitable Investors, Koyfin Cisco v Nvidia in terms of market cap and net income (net profit)

Source: Koyfin US real GDP growth contribution from tech capex

Source: JP Morgan Bridgewater Power demand from AI data centres to quadruple in 10 years according to Bloomberg

Source: Bloomberg NEF The first time an Australian company enters external administration or has a controller appointed - monthly

Soure: ASIC Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

10 Oct 2025 - Hedge Clippings |10 October 2025

|

|

|

|

Hedge Clippings | Friday, 10 October 2025

News | Insights When Regimes Shift, So Should Portfolios | East Coast Capital Management Plans are worthless but planning is essential | Canopy Investors September 2025 Performance News Bennelong Australian Equities Fund Quay Global Real Estate Fund (Unhedged) |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

10 Oct 2025 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]

10 Oct 2025 - Performance Report: Quay Global Real Estate Fund (Unhedged)

[Current Manager Report if available]

10 Oct 2025 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

10 Oct 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| TAMIM Global Infrastructure Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| ASCF Private Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Metrics Real Estate Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

|

||||||||||||||||||||||

| Pantheon Global Private Equity Fund (PGPE) | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

9 Oct 2025 - Geopolitics - Markets to take a backseat, investors need not do the same

|

Geopolitics - Markets to take a backseat, investors need not do the same Janus Henderson Investors September 2025 Jay Sivapalan, Head of Australian Fixed Interest, discusses the impact of geopolitical shifts on global economic dynamics, emphasising the need for investors to realign with government strategic priorities. Timely & Topical Geopolitical issues are currently having a heavy influence on economic and market outcomes. Global tectonic shifts are occurring in the areas of trade, defence, energy, technology and a desire for national resilience. Consequently, the key pillars that drove synchronised global economic growth are under threat with economic growth drivers such as the peace dividend we've enjoyed over the last 80 years and free trade agreements we've appreciated for decades, no longer intact. Whilst we in the investment community would like to think markets are central to government actions, the harsh reality is that they are not. The market feedback mechanism is important in governments achieving their economic and geopolitical objectives. However, higher order priorities for governments are increasingly apparent. For much of the past four or five decades, investors have been able to rely on some simple principles for investing within free market based capitalist economies. The allocation of scarce resources was driven almost solely by the highest return on capital available, feedback from market pricing and free competition anchored by comparative advantage. The role of government mostly centred around delivery of public goods and services, provision of safety nets as well as keeping checks and balances in place through regulation. An environment where private sector decisions ultimately drove markets whilst governments played a supportive role. Markets were at the forefront of these private sector (and some public sector) decisions. Looking ahead, we see the potential for the roles of government and the private sector to be reversed. Where governments have strategic priorities driving critical decisions around the use of capital, labour, technology and other scarce resources dictating the growth or fall in certain sectors, the higher order priority now is to achieve nationalistic objectives. While the private sector will absolutely be necessary for governments to achieve their more strategic goals, the bigger picture decisions are not likely to be driven by free market pricing signals per se. Going forward, the role of the private sector, whilst different and not in the driving seat, remains critical to governments achieving their objectives. The main reason being that the intellectual property, investor capital, skilled labour and track record of delivery sits within the private sector. Governments also absolutely need the private sector to execute their objectives. Therefore, key success factors for private sector participation will be:

Thinking differentlyThe geopolitical environment over the coming decades will be significantly different to the past. The historical norm of shooting for comparative advantage in trade is one case in point. Countries specialising in producing and exporting goods and services for which they have a lower production cost compared to others, enables greater total production and consumption than otherwise achieved in isolation. This is at the heart of globalisation and global commerce. In a controlled environment, a constrained optimum, a framework that delivers the benefits of comparative advantage can still hold but the level of complexity increases. Regulation, resource availability, technological factors and social and political objectives have always been in the frame as constraints. Increased nationalist and protectionist policies can add further distortion and friction to otherwise economically rational decisions which have sharpened the focus of governments and their policy makers. For investors, the implications are that the economy and markets are no longer front and centre in policymakers thought processes. Rather, markets are a tool through which economies and their respective governments to achieve their strategic priorities. Protectionist policies, for example, may mean that there's no certainty a trading partner can be relied upon to maintain willingness/capacity to deliver goods and services as required. Instead of an optimally efficient economic outcome being pursued, higher order government policies may take precedent. That is, governments may no longer pursue the cheapest option, but that with the greatest certainty of execution. The outcome is that winners and losers will emerge and the gulf between each is likely to expand. Governments will be much more influential in who those winners and losers are at the country, industry and company level. Investment implications - There will be winners and losersFor investors, the playbook for success has changed. Identifying the strategic priorities for governments and the number one, two and three operators with a track record of successful execution in these areas is a good start. Determining which industries could receive subsidies and tax breaks could also prove advantageous. As a guide, investors would be well served to assess investments with a focus on:

This shift in approach from starting with the private sector to now commencing with governments' strategic priorities, whilst it may change the way industries and companies will succeed or fail, does not preclude successful investing and strong returns on invested capital across a range of asset classes. There will be winners and losers! Companies poised to benefit from strategic priorities such as the following are worth exploring:

A way forwardClearly, investors need to think and allocate differently to how they have in the past and will need to work portfolios harder and more diligently to achieve their objectives. Pursuing similar return targets to those achieved previously but in a safer way may be the better way to go, rather than leaning into risk which has been so well rewarded. For example, to maintain purchasing power and grow a corpus in real terms, pension funds, endowments, foundations and insurance companies often target CPI + 3%. Currently, investors are better able to avoid leaning as heavily into growth assets to achieve these objectives, with a greater allocation to defensive assets possible. The past year has proven this to be the case with fixed income reestablishing itself as a compelling opportunity to drive attractive returns. The full gamut of options have delivered attractive return outcomes. Investment grade credit, the sweet spot between traditional equities and more pedestrian cash where risk of default, especially in Australia, is remote and has delivered 7.8% returns for FY25*, close to long term assumptions for equity market returns in asset allocation models. Investing differently for successful outcomesThe world is changing rapidly and for policymakers, markets are not the primary focus. Investors can still succeed but need to change the way they invest. When assessing policy and geopolitics, it is more relevant to back solve for what is firstly in the best interests of a nation and its public objectives, then the economy and markets - it's simply a different playbook. Just because markets have taken a back seat to geopolitics doesn't mean investors have to do the same. Many of the higher order government objectives will need to be delivered by the private sector. And with potentially government supported policy, regulation, subsidies, discounted funding and equity backing. Successful investment outcomes are very likely but achievable investing through a different lens. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund , Janus Henderson Net Zero Transition Resources Fund *Bloomberg AusBond Credit 0+ Yr Index, as at June 2025. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

8 Oct 2025 - Plans are worthless but planning is essential

|

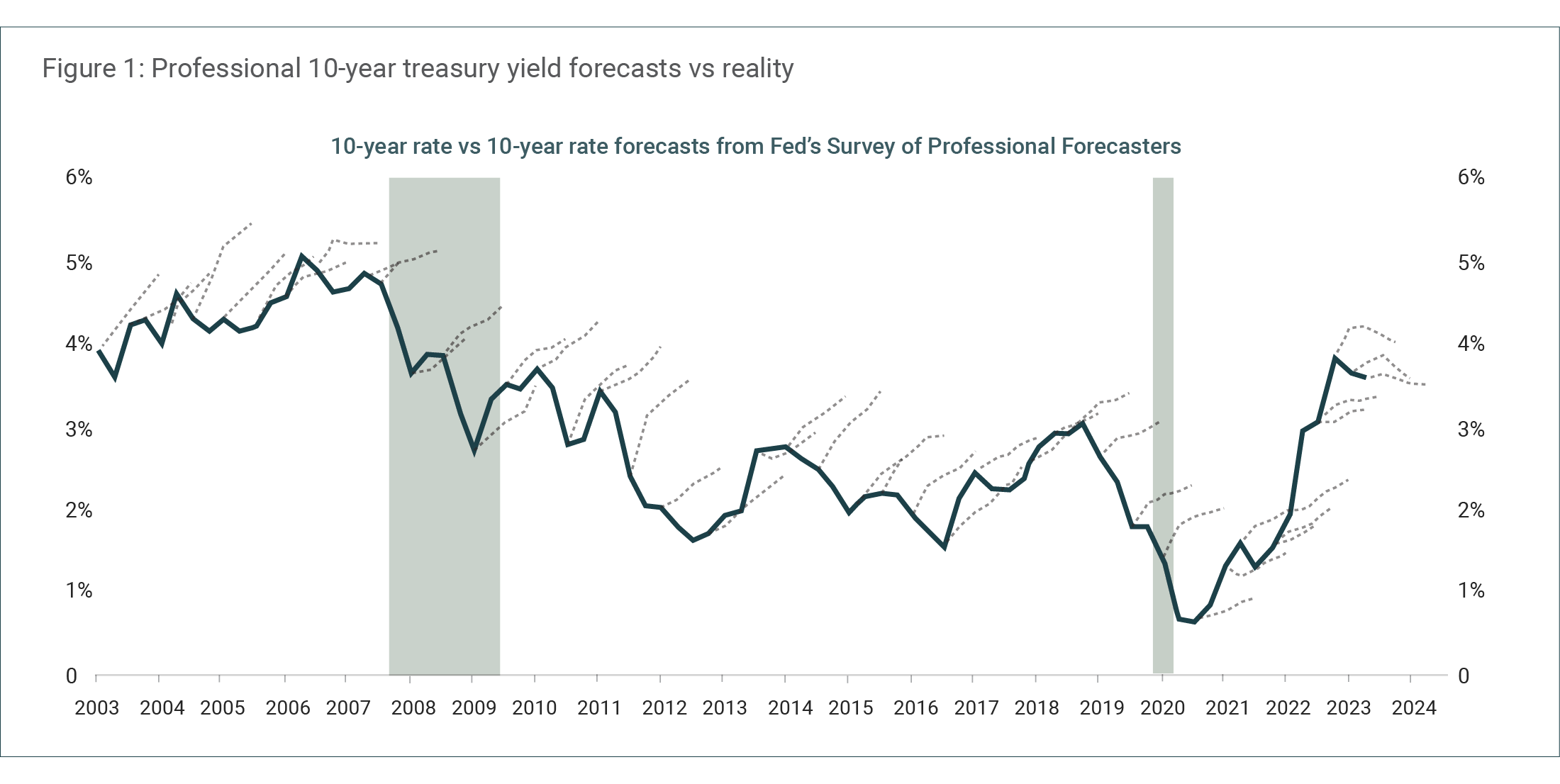

Plans are worthless but planning is essential Canopy Investors September 2025 5 min read 'Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.' Warren Buffett has previously observed that for information to be useful in investing, it must be both important and knowable. While macroeconomic outcomes are undeniably important, evidence suggests they cannot be predicted with useful accuracy. The forecasting fallacyThe track record of professional macro forecasting is remarkably poor. Prakash Loungani's 2001 study analysed consensus GDP growth forecasts from private sector economists across sixty-three countries, examining sixty recessions from 1989 to 1998. His analysis showed that only two of the sixty recessions were predicted a year in advance, two-thirds remained undetected by April of the recession year, and in about a quarter of cases forecasters were still predicting positive growth in October of the recession year. As Loungani concluded, "the record of failure to predict recessions is virtually unblemished." Major institutions perform no better despite employing teams of PhD economists and having privileged access to non-public information. Andrew Brigden of Fathom Consulting examined International Monetary Fund (IMF) predictions across 194 countries, analysing 469 economic downturns from 1988 to 2018. The IMF successfully predicted only four recessions a year in advance - a success rate of just 0.85% - with all successful predictions involving smaller developing economies rather than major markets. This pattern extends beyond recessions to other key macro variables. Figure 1 below shows two decades of professional interest rate forecasts consistently overestimating future yields and missing every major decline.

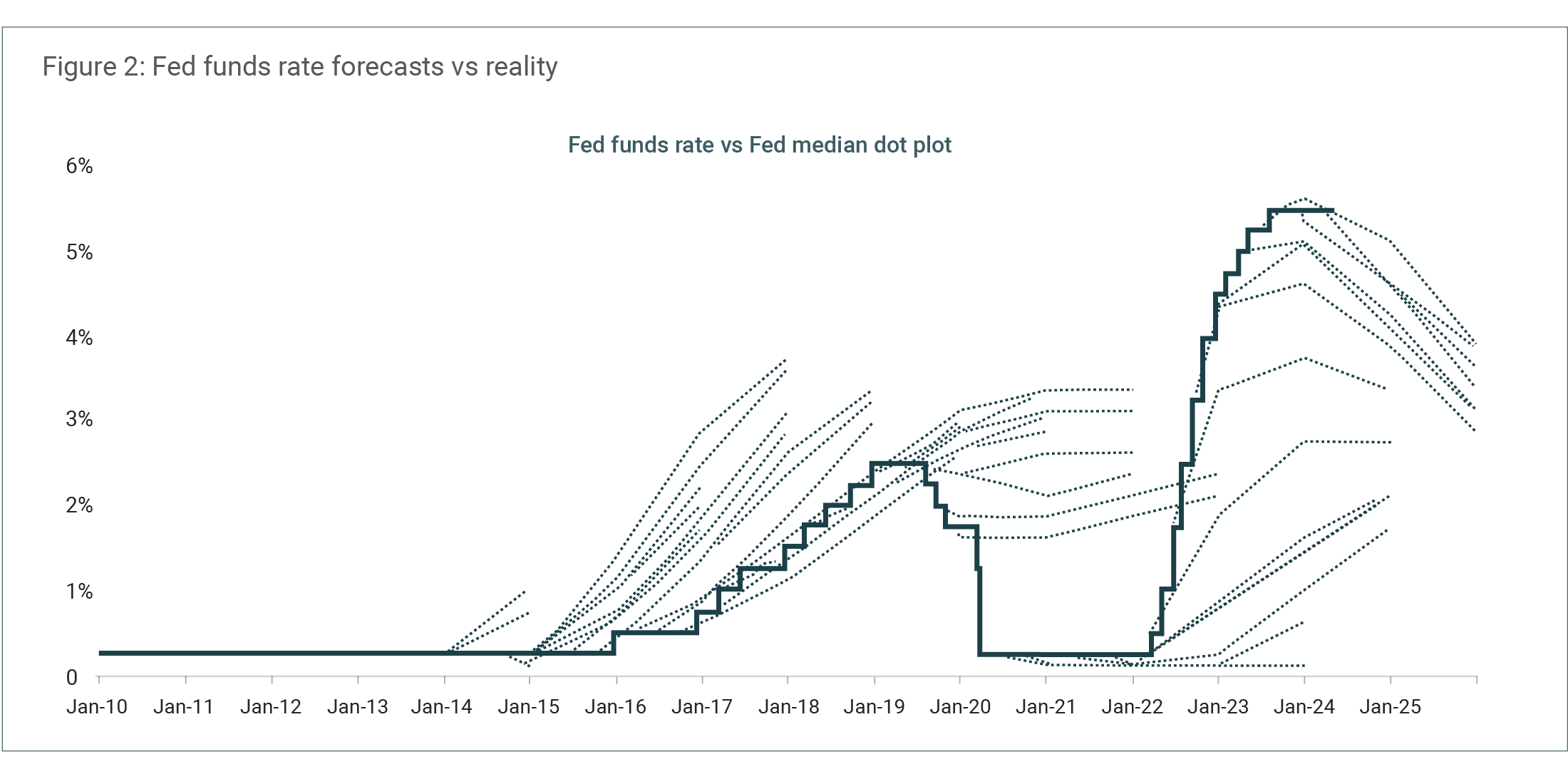

Source: Bloomberg, Philadelphia Fed Survey of Professional Forecasters, Apollo Chief Economist. Tellingly, the Federal Reserve struggles to predict even its own policy decisions. Figure 2 below highlights how Fed officials' projections of the funds rate (a metric they directly control) consistently miss the mark by wide margins.

Source: FOMC, Bloomberg, Apollo Chief Economist. The double prediction problemImagine that you could predict every recession, every inflation spike, and every policy change. Would you be guaranteed investment success? The surprising answer is no. As Howard Marks explains, "Even if you somehow manage to get an economic forecast correct, that's only half the battle. You still need to anticipate how that economic activity will translate into a market outcome. This requires an entirely different forecast, also involving innumerable variables, many of which pertain to psychology and thus are practically unknowable." We see this challenge in action when identical economic news can drive markets in unpredictable, sometimes opposing directions depending on prevailing sentiment, prior expectations, and what's already priced in. Lower inflation could spark a rally (rate cuts ahead!) or trigger selling (economic weakness!). The recent inflation cycle illustrates this perfectly. Economists consistently underestimated how aggressively the Fed would raise rates to combat inflation, forecasting a peak Fed funds rate in 2022 of around 3.5% when it actually reached 5.25-5.50%. Yet even perfect rate forecasting wouldn't have helped predict the subsequent market behaviour. Basic finance theory suggests higher rates should pressure valuations, but the S&P 500 has hit repeated record highs since then, powered most recently by optimism around artificial intelligence. Perfect economic forecasting, in other words, is only half the challenge. |

|

Funds operated by this manager: |