NEWS

Investment Perspectives: A big disinflation tailwind is coming

With the US economy showing signs of accelerating growth despite rising interest rates, Chris Bedingfield discusses the impact of shelter costs in driving disinflation.

Read more...

Hedge Clippings | 29 September 2023

Although some sections of the media attempted to make a big deal of it, Wednesday's headline annual inflation rate for August, which came in at 5.2%, up from 4.9% the previous month, was both widely expected, and no cause for the RBA to...

Read more...

Performance Report: Insync Global Quality Equity Fund

The Insync Global Quality Equity Fund rose by +0.96% in August, outperforming the All Countries World (AUD) benchmark by +2.16%. Since inception in October 2009, the fund has returned +12.43% per annum, an outperformance of +1.41% relative...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +3.37% in August, outperforming the ASX 200 Total Return benchmark by +4.1%. Since inception in January 2013, the fund has returned +12.8% per annum, an outperformance of +4.05% relative to the benchmark...

Read more...

The Rate Debate - Ep 42: Inflation has peaked

Outgoing Reserve Bank governor Philip Lowe finished his tenure as he began by keeping rates on hold as inflation cools.

With inflation past its peak, can we expect rate cuts on the horizon, and could a softening of China's...

Read more...

Performance Report: Insync Global Capital Aware Fund

The Insync Global Capital Aware Fund rose by +0.94% in August, outperforming the All Countries World (AUD) benchmark by +2.14%. Since inception in October 2009, the fund has returned +10.5% per annum, a difference of -0.52% relative to...

Read more...

Climate Finance Strategies and Global Decarbonisation

The success of global decarbonization relies on climate finance, which directs financial resources towards combating climate change through renewable energy, energy efficiency, and emission reduction projects. Decarbonization aims to...

Read more...

Performance Report: PURE Resources Fund

The PURE Resources Fund rose by +0.1% in August, outperforming the S&P/ASX Small Industrials TR benchmark by +0.96%. Since inception in May 2021, the fund has returned +8.36% per annum, an outperformance of +5.35% relative to the benchmark...

Read more...

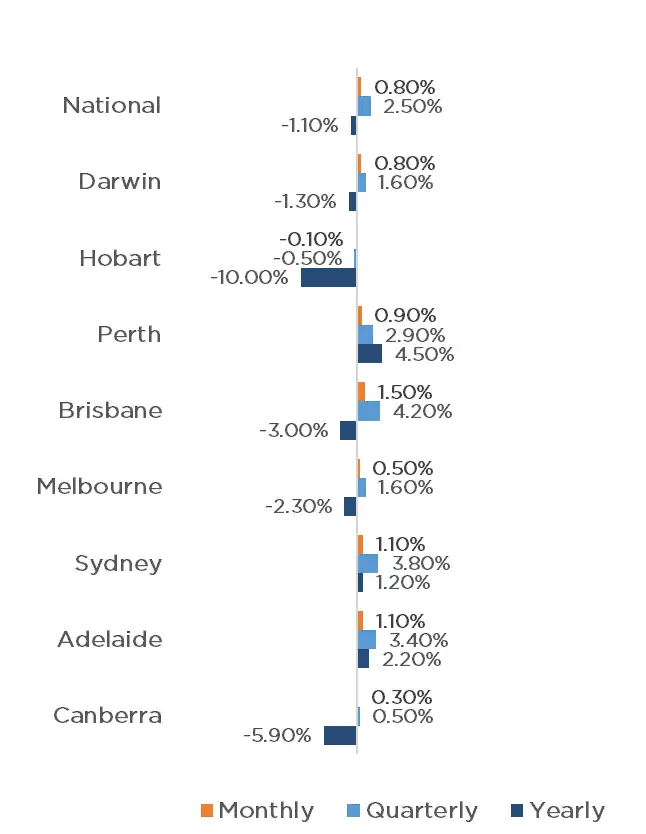

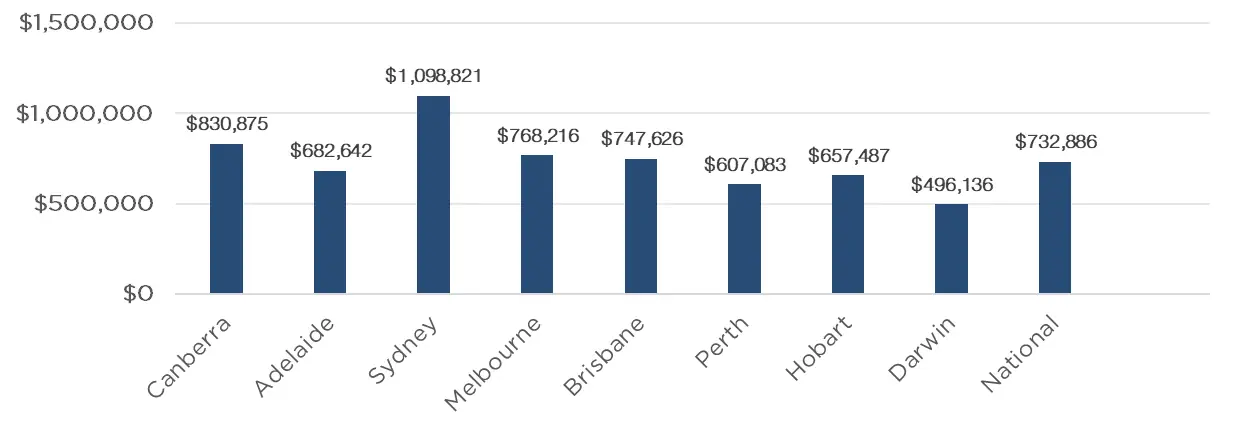

Australian Secure Capital Fund - Market Update

The RBA has elected to maintain the current cash rate for the third month in a row, with economists predicting we are at the top of the interest rate cycle. This is a positive sign for Australian property prices, as consumer confidence...

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund rose by +0.71% in August, outperforming the ASX 200 Total Return benchmark by +1.44%. Since inception in November 2009, the fund has returned +9.57% per annum, an outperformance of +1.78%...

Read more...