NEWS

Performance Report: Delft Partners Global High Conviction Strategy

The Delft Partners Global High Conviction Strategy rose by +0.19% in May. Since inception in August 2011, the strategy has returned +14.26% per annum, a difference of +1.62% relative to the All Countries World (AUD) benchmark which has...

Read more...

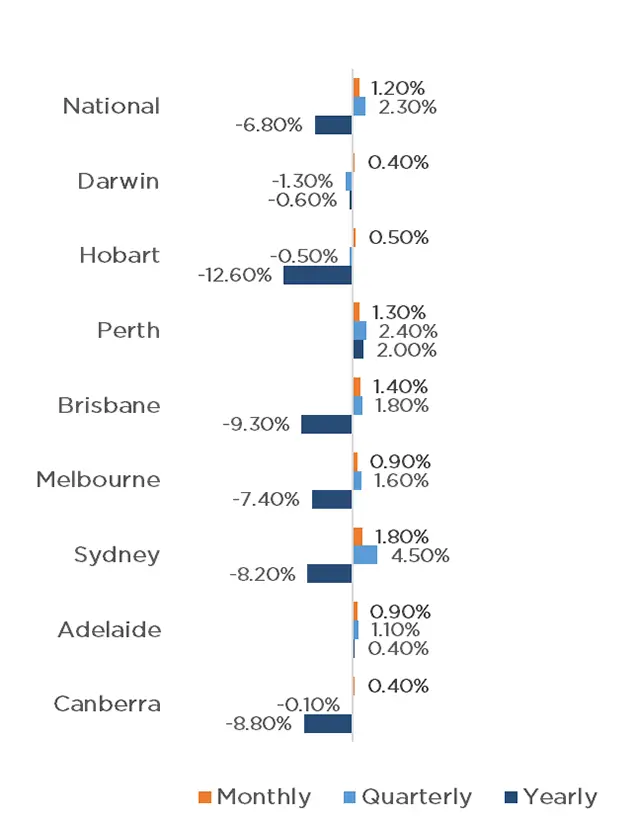

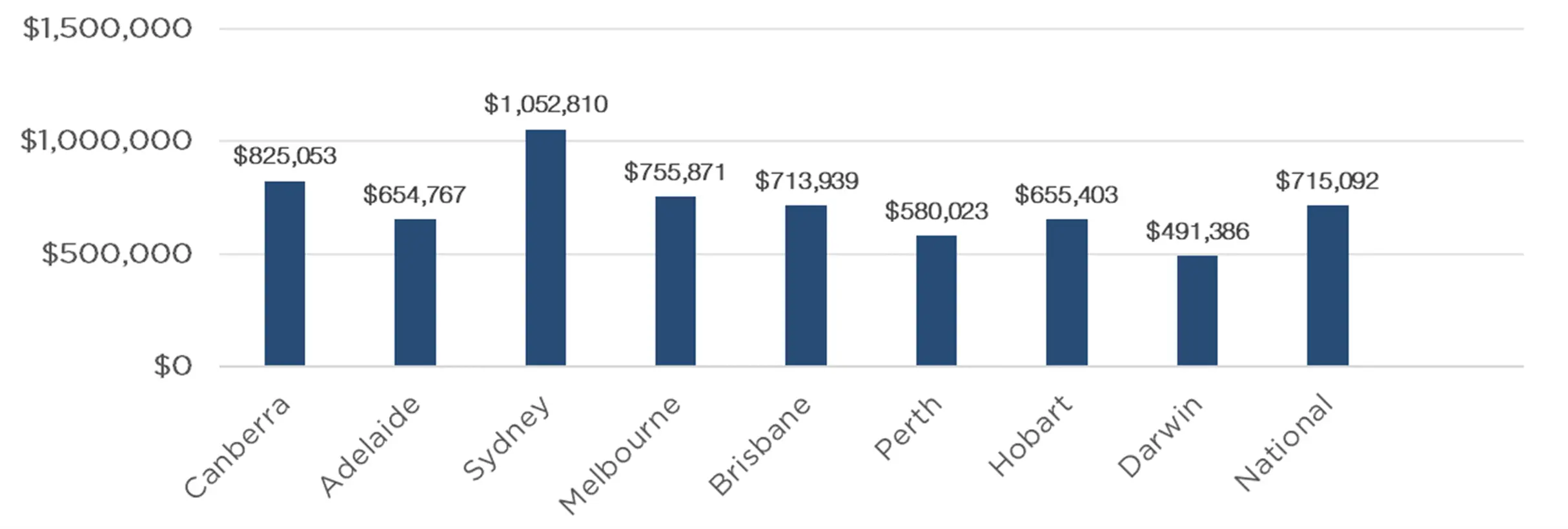

Australian Secure Capital Fund - Market Update May

The Australian housing market continues to bounce back despite further interest rate rises, with CoreLogic's national Home Value Index rising by 1.2% in May.

Read more...

Performance Report: PURE Resources Fund

The PURE Resources Fund rose by +0.26% in May, an outperformance of +7.44% compared with the S&P/ASX Small Resources TR benchmark which fell by -7.14%. Since inception in May 2021, the fund has returned +7.51% per annum, a difference of...

Read more...

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) returned -2.97% in May, an outperformance of +0.62% compared with the S&P Global Infrastructure TR (AUD) benchmark which fell by -3.59%. Since inception in March 2016, the fund has returned...

Read more...

Hedge Clippings | 16 June 2023

Inflation: No Pain, No Gain.

Paul Keating will long be remembered for his "recession we had to have" comment, made way back in 1990. The self-styled "World's Greatest Treasurer" embraced the attention the comment gave him at the...

Read more...

Performance Report: ASCF High Yield Fund

The ASCF High Yield Fund rose by +0.55% in May, an outperformance of +1.76% compared with the Bloomberg AusBond Composite 0+ Yr benchmark which fell by -1.21%. Since inception in March 2017, the fund has returned +8.29% per annum, a...

Read more...

Performance Report: Collins St Value Fund

Since inception in February 2016, the Collins St Value Fund has returned +12.59% per annum, a difference of +3.33% relative to the ASX 200 Total Return benchmark which has returned +9.26% on an annualised basis over the same period.

Read more...

Glenmore Asset Management - Market Commentary

Equity markets were mixed in May. In the US, the S&P 500 rose +0.3%, the Nasdaq rebounded sharply +5.8%, whilst in the UK, the FTSE 100 declined by -5.4%. In Australia, the All Ordinaries Accumulation index fell -2.6%, driven by ongoing...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund returned -2.22% in May, an outperformance of +0.31% compared with the ASX 200 Total Return benchmark which fell by -2.53%. Since inception in January 2013, the fund has returned +12.01% per annum, a difference of...

Read more...

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund returned -1.55% in May, an outperformance of +0.98% compared with the ASX 200 Total Return benchmark which fell by -2.53%. Since inception in June 2018, the fund has returned +9.71% per annum, a difference...

Read more...